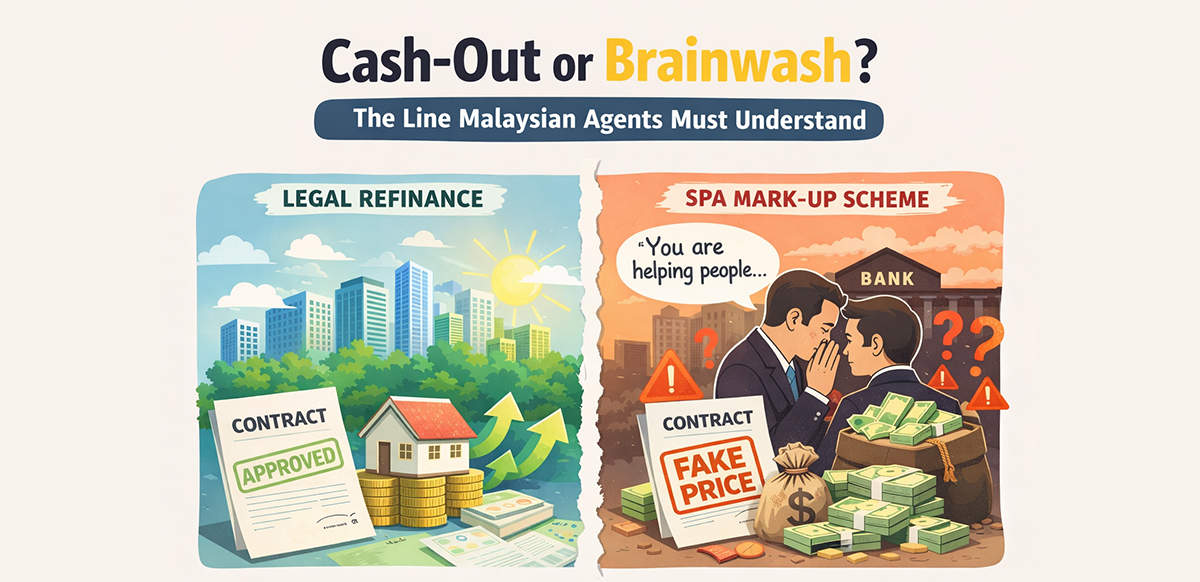

Cash-Out or Brainwash? The Line Malaysian Agents Must Understand

The Emotional Hook: “You Are Helping People”

In parts of the Malaysian property market, junior negotiators are sometimes introduced to what is framed as a “cash-out strategy.”

When they hesitate about marking up the SPA price to obtain higher loan disbursement, the reassurance they receive is rarely technical. It is emotional.

They are told:

- “You are helping people.”

- Clients are burdened by high-interest credit card debt.

- Personal loans are expensive.

- Business cash flow may be tight.

They are also reminded that housing loan interest rates are lower and that by facilitating this structure, they are improving the client’s financial position.

The phrase is powerful because it appeals to morality rather than mechanics. No junior wants to feel unethical. When the structure is framed as compassion, resistance weakens.

The conversation shifts:

- Away from whether the declared transaction value reflects reality

- Toward whether the client benefits from the outcome

The moral evaluation becomes outcome-based rather than truth-based.

However, intention does not replace mechanism.

The Legal Version: Genuine Appreciation and Refinance

There is absolutely nothing wrong with cashing out through legitimate refinancing.

If a property has genuinely appreciated in value, the owner may refinance based on current market valuation conducted independently by the bank.

Example:

- Property purchased at RM500,000

- Current market value assessed at RM700,000

- Bank valuation supports the increase

The owner refinances and extracts part of the equity created by real appreciation.

If the funds are used to consolidate higher-interest debt or support business liquidity, the structure remains clean because it is supported by independent verification and truthful declaration.

In this structure:

- No numbers are manipulated

- The bank understands the exposure

- The valuation reflects actual market conditions

The client benefits, but the benefit is built on accurate representation.

This is legal cash-out.

It does not require moral justification because it stands on factual valuation.

The Illegal Version: Artificial SPA Mark-Up

The problem arises when the SPA price is intentionally inflated beyond true market value in order to influence the loan amount.

In such cases, the declared transaction price does not reflect reality.

The justification may still revolve around helping the client reduce interest burden, but the structure depends on misrepresentation.

Lower interest rates do not legalize false numbers.

The comparison between housing loans and personal loans does not change whether the declared price is accurate.

When the transaction value is engineered rather than supported by independent valuation, the foundation of the deal shifts:

- From financial strategy

- To distortion

The difference between refinancing after appreciation and marking up an SPA is not minor.

- One relies on independent assessment

- The other relies on coordinated inflation

One is valuation-based. The other is declaration-based.

These are fundamentally different mechanisms.

The Market Reality: “No One Gets Into Trouble”

In Malaysia, the junior negotiator’s name is typically not printed as a contracting party on the SPA or loan agreement.

The legal relationship exists between:

- Buyer and seller

- Borrower and bank

Because of this, many juniors believe they carry minimal exposure.

If the bank discovers the inflated value, the most common outcome may simply be loan rejection rather than prosecution.

This perception contributes to normalization.

When enforcement appears inconsistent and consequences seem limited, ethical evaluation shifts:

- From “Is this correct?”

- To “Will anything happen?”

The act becomes measured by probability of detection rather than structural honesty.

But professional standards are not defined by enforcement frequency.

They are defined by whether the declared information is truthful.

Even if no immediate action is taken, normalization reshapes industry culture.

Where Brainwashing Happens

The most subtle aspect of this issue lies in psychological framing.

When juniors question the structure, they may be told:

- They are inexperienced

- They are overly rigid

- The client benefits anyway

- Banks still earn interest

The explanation often becomes comparative:

- Housing loan interest is lower than personal loan interest

- The client’s financial burden becomes lighter

Instead of asking whether the transaction value reflects market reality, the conversation shifts to whether the client’s financial position improves.

The moral compass shifts from compliance to compassion.

This is how brainwashing operates.

It reframes misrepresentation as assistance.

Once that shift occurs, ethical lines begin to blur.

Why the Distinction Matters

Malaysia’s property industry already operates within an environment of cautious trust.

Banks monitor risk carefully and regulators tighten processes when irregularities accumulate.

When artificial mark-ups become normalized under the banner of helping clients, the long-term cost is borne by the entire profession.

In contrast, genuine refinancing after appreciation strengthens financial sophistication.

It:

- Respects valuation processes

- Aligns with banking policy

- Requires no defensive narrative

It does not rely on emotional reassurance.

If a structure repeatedly requires the explanation “you are helping people,” it may signal that the mechanism itself cannot stand comfortably on its own.

The Clear Line

Cash-out is not inherently unethical.

Legal refinancing based on genuine market appreciation is a legitimate financial strategy.

Debt consolidation conducted through transparent valuation is responsible advice.

Artificially inflating the SPA price to extract additional loan is not the same thing.

It is misrepresentation regardless of intention.

Helping people and telling the truth must exist together.

If helping someone requires distorting declared value, the help is built on an unstable foundation.

The line is not blurry.

- If appreciation is real and independently valued, refinance is smart

- If price is engineered to influence loan outcome, it is distortion

Understanding this distinction protects professional integrity and long-term credibility.

The difference is clear. The responsibility to maintain that clarity belongs to every agent who wants the industry to mature.