The Unspoken Housing Risk: What Happens to Property Demand If a Generation Stops Getting Married?

For decades, housing demand was driven by a predictable life script:

Study → Work → Marry → Buy Home → Have Kids → Upgrade Home

But what if the next generation no longer follows that script?

The question is no longer just “Can young people afford property?”

It is becoming:

“Does a generation that delays or rejects marriage still need the kind of housing the market is built on?”

This is not a theory — it is a demographic shift already visible in Japan, South Korea, China, Singapore, Europe, and increasingly, Malaysia.

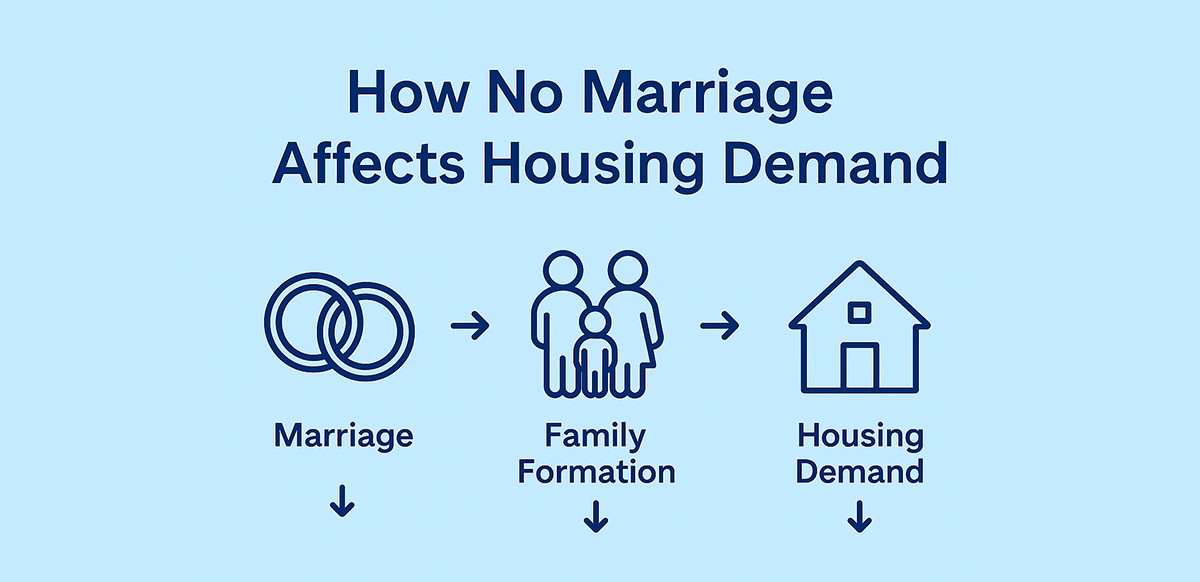

Marriage Was the Engine of Housing Demand

In most societies, new household formation came from marriage:

Two people leave their parents' homes

They merge income and buy their first property

They upgrade when children arrive

They eventually move into a larger, longer-term home

If marriage slows or stops, the automatic demand trigger for housing disappears.

Housing demand becomes discretionary, not guaranteed.

Why Fewer People Are Choosing Marriage — A Multi-Sided Shift

This issue is not simply “men can’t afford marriage” or “women are too demanding.” The traditional logic of marriage has broken down for both genders — economically, socially, and culturally.

1. Stagnant Wages vs Rising Living Costs

Income growth has not kept up with the cost of housing, childcare, food, and education. Young adults are asking:

“If I cannot afford a stable future, why commit to marriage at all?”

2. Housing as a Prerequisite for Marriage

In previous generations, marriage came first, home ownership later. Today, many treat property as a condition for marriage:

“If you do not own a home, you are not ready to marry.”

When home ownership becomes a filter, marriage rates fall in parallel with housing affordability.

3. Women Can Now Afford to Remain Single

A rising share of women now:

- Earn their own income

- Qualify for loans independently

- Buy property on their own terms

- Do not require marriage for financial stability

Marriage has shifted from economic necessity to optional lifestyle choice.

4. Careers and Self-Fulfilment First

Both men and women are prioritizing:

- Higher education

- Career progression

- Global mobility and travel

- Entrepreneurship or freelance work

- Personal development

By the time they reach “financial stability,” the traditional marriage window has passed.

5. Marriage Is Now Evaluated Like a Legal Contract

Many young adults view marriage in risk-adjusted terms:

- High upfront cost (wedding, house, renovation)

- Legal and financial exposure in divorce

- Single-income mortgage risks

- Potential asset split or alimony concerns

Marriage is no longer automatically seen as a life upgrade, but as a high-commitment, high-liability financial decision.

The New Housing Reality: Demand Isn’t Vanishing — It Is Changing Form

| Old Housing Assumption | New Housing Reality |

|---|---|

| Marriage triggers first home purchase | Housing is independent of marital status |

| 3-bedroom suburban units | Smaller, urban, flexible units |

| Buy → upgrade → retire | Rent, co-own, invest, stay mobile |

| House = family foundation | House = personal security or lifestyle asset |

New household types are emerging:

- Dual Income, No Kids (DINKs)

- Friends or siblings co-buying property

- Single professionals buying 1-bedroom + study units

- Long-term renters with high savings and career mobility

The “family home” may no longer be the dominant property category.

The Real Estate Domino Effect

If marriage and birth rates continue to decline, the industry will experience shifts:

| Impact Area | Likely Outcome |

|---|---|

| Developer product focus | Smaller, flexible, lifestyle-based units |

| Suburban family housing | Slower take-up and rising vacancy |

| Interior layouts | More home offices, fewer nurseries |

| Rental market | Higher demand from long-term singles and DINKs |

| Mortgage patterns | More single-name loans, fewer joint mortgages |

| Retail ecosystem | Decline in child-centric suburban retail |

| Build-to-Rent | Becomes more relevant as long-term renting normalizes |

The property market has long assumed one certainty:

There will always be new families, therefore there will always be new housing demand.

That assumption is no longer safe.

Final Thought

The biggest risk to future housing demand may not be interest rates, economic slowdown, or construction cost — but something cultural:

A generation that no longer sees marriage and home ownership as necessary life milestones.

The key question for the real estate industry is shifting:

Not:

“How do we make property affordable for young buyers?”

But:

“What happens to the housing market when the traditional purpose of owning a home disappears?”